WGA Bank Top 50 Q2 2026 | Bank Failures and Mortgage Bankers

- May 3

- 7 min read

Updated: May 4

"Suppose you were an idiot. And suppose you were a member of Congress. But I repeat myself…. There is no distinctly American criminal class—except Congress."

Mark Twain

May 4, 2026 | This week The Institutional Risk Analyst celebrates the one-year anniversary of the publication of the Second Edition of “Inflated: Money, Debt and the American Dream” by our friends at John Wiley & Sons. The message of Inflated is very simple: Americans don’t like paying taxes and the Congress, being democratically elected, is comprised of invidious cowards unwilling to make tough decisions. As Americans, we pay our way via continuous currency inflation, yet in doing so have created the world's default means of exchange and also finance. This suggests a barbel strategy to prudent investing that we’ll address in a future comment.

FDIC Promptly Resolves Second Bank Failure

Last week, Community Bank and Trust - West Georgia of LaGrange, Georgia was closed by the Georgia Department of Banking and Finance, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. The FDIC acted as per the Depression era laws that facilitate bank resolutions and literally saved the country from a forced liquidation a 110 years ago

The creation of the FDIC as the first federal receiver in 1933 enabled the restructuring of the US economy. In particular, FDIC allowed Federal Reserve Banks to lend to solvent member banks in a meaningful way. Wisconsin businessman Leo Crowley at the FDIC and Houston business giant Jesse Jones at the Reconstruction Finance Corp proceeded to restructure thousands of banks and the US economy and, later, prepare for war.

Both men served the United States through WWII. As FDIC Chairman, Crowley focused on stabilizing the banking system by strengthening capital structures and eliminating weak, unsound banks, rather than merely bailing them out. He urged banks to adopt a "10-to-1" deposit-to-capital ratio, advocating that banks sell capital stock or notes to the Reconstruction Finance Corporation (RFC) to improve solvency and public confidence. Crowley later ran war finance for the FDR Administration.

Last week, the Crowley designed FDIC entered into an agreement with Anchor Bank of Palm Beach Gardens, Florida to assume substantially all insured deposits and acquire certain assets of Community Bank and Trust - West Georgia, which had $288 million in total assets at the end of 2025. FDIC currently estimates that the failure of Community Bank and Trust, which is located on the I-85 corridor between Atlanta and Montgomery, will cost its Deposit Insurance Fund approximately $97 million or one-third of total assets.

Why did the bank fail? Realized losses related to construction loans, farm land and owner-occupied commercial loans. The bank had almost 6% of total assets in non-performing loans, a Texas ratio of 150% at year-end 2025 and did not file a call report in Q1 2026. But any banker will tell you that real estate exposures along the endless highways of Georgia can be treacherous places to extend credit. But big hat tip to FDIC for another prompt resolution. The lesson of Silicon Valley bank is that insolvent institutions are sold immediately.

UWMC Raises Bid for Two Harbors

Meanwhile in the world of mortgage finance, United Wholesale Mortgage Corp (UWMC) audaciously issued an open letter to the stockholders of Two Harbors Investment Corp. (TWO) last week. The letter sets out why UWMC’s believes that the new $12 per share offer is clearly superior to Two Harbors’ proposed transaction with private Cross Country Mortgage.

At present, TWO is trading just north of $12 per share for a market capitalization of about $1.3 billion. Yet TWO owns a mortgage servicing right (MSR) with a fair value over $2.2 billion. What gives? Sad to say, TWO has a $1.3 billion negative book value due to mark-to-market losses on its mortgage-backed securities (MBS) portfolio from rising interest rates and widening spreads, a disastrous $375 million litigation settlement, high operating expenses, and extensive share buybacks.

Which deal is better? To us, holders of TWO should pick the highest cash offer available, whether from wholesale giant UWMC or retail leader Cross Country. We like the LT prospect of Cross Country better than UWMC because of the lower leverage and more rational business model. Like some other large lenders, UWMC has been waiting for lower mortgage interest rates to drive up lending volumes and essentially dig their way out of a hole. But rates may rise from here.

Source: dataQollab

We’ve written about the eye-watering corporate debt at UWMC (“Countrywide II: UWMC + TWO = ? Loan Depot Flops, Again”), net of secured debt for loan production. When a non-bank lender has a lot more unsecured debt than MSR, that’s bad. The levels of leverage at UWMC have caught the attention of the mortgage finance industry.

More, at below $5 per share, UWMC has zero collateral value, another reason why TWO holders should stick with Cross Country. Remember, the MSR is the net present value of future cash flows. Imagine what Leo Crowley would say about an intangible, negative duration MSR in a discussion about bank solvency? Banks did not book intangibles period in 1933.

When a non-bank lender like UWMC is selling MSRs at a discount to the cost of creation to offset operating losses, that’s even worse in our book. The more astute players in the industry retain the MSR, finance the asset in the bank and HY debt markets, keep MSR hedge costs to a minimum, and spend their cash creating new servicing assets. To us, creating MSRs on a ~ 6x multiple because your bid for loans in the wholesale channel is totally excessive, then selling the servicing at a discount to raise cash is not a viable model LT.

UWMC 10-K February 2026

We’d like to see UWMC back off their bid a tad for new loans and retain the MSR, but it may already be too late for such prudent counsel to change the ultimate outcome we’ve warned about for several years. Trouble is, unlike Countrywide which was acquired by Bank of America (BAC) in mid-2008, none of the secured bank lenders to UWMC including Goldman Sachs (GS) and Citigroup (C) are likely to purchase the largest non-bank lender in the US when they stumble.

The WGA Bank Top 50

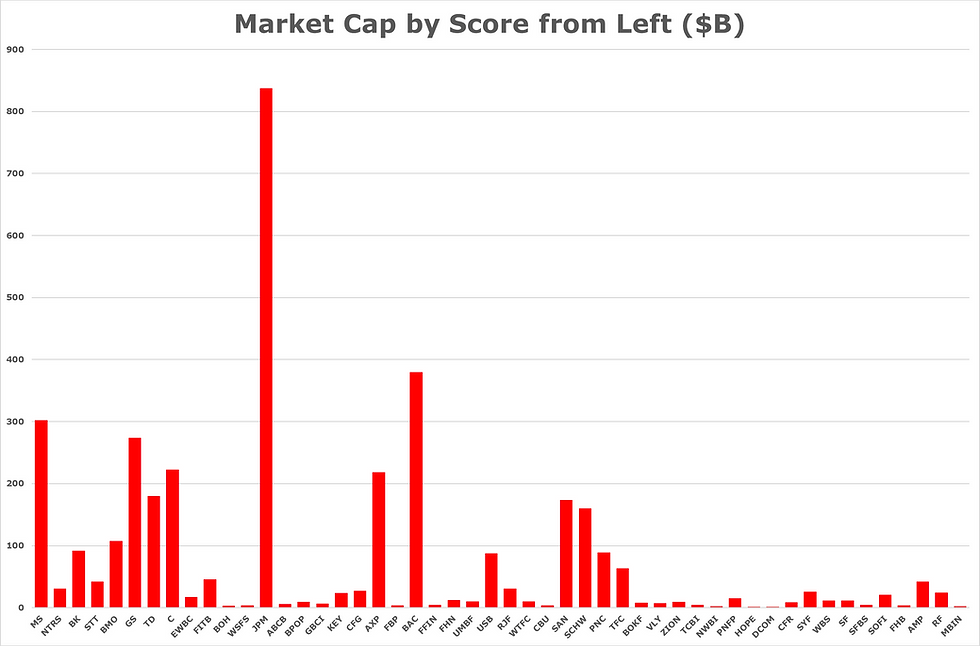

The results for the WGA Bank Top 50 reflect market conditions, with some of the larger banks in the industry far down on the list. The top-ranked bank in Q2 2026 among the 99 publicly traded banks in our test group was Morgan Stanley (MS) followed by Northern Trust (NTRS) and Bank of New York Mellon (BK). NTRS was #2 last quarter as well and BK moved up from #9 in Q1.

MS had a total score of 459 out of a maximum possible score of 495. The chart below shows the distribution of banks by market cap starting from the highest score for MS at left.

WGA Bank Top 50 | Q2 2026

Source: Yahoo Finance/WGA LLC

Some notable observations from the group include:

JPMorgan rose to #13 from 44th in Q1 2026.

Citigroup rose to #8 in Q2 from 16th in Q1 2026 due to continued strong market performance, but notice the tiny market cap vs JPM.

State Street (STT) rose from 13th in Q1 2026 to #4 in Q2 2026.

The Toronto-Dominion Bank (TD) rose from 30th in Q1 2026 to #7 in Q2.

Of course, in the muddled markets at present, there are a number of low-scoring banks which have done relatively well in recent weeks. The parent company of tiny Merchants Bank of Indiana, Merchants Bancorp (MBIN), for example, saw its stock price rise significantly in early 2026, 2x the S&P 500 over the past year, driven primarily by its inclusion in a major index and strong financial performance. We've written positively about MBIN in the past, yet based upon size and the qualitative factors in our test, the overall score ended up at 50th.

Subscribers to the Premium Service may login to view the Bank Top 50 and the entire 99 bank test group on our website, down from 101 subjects in Q1 2026. Comerica Incorporated was acquired in an act if supreme generosity by Fifth Third Bancorp (FITB), and Two Rivers Financial Group was acquired by First Mid Bancshares (FBMH).

We will be updating The WGA Precious Metals Top 25 this week.

The Institutional Risk Analyst (ISSN 2692-1812) is published by Whalen Global Advisors LLC and is provided for general informational purposes only and is not intended for trading purposes or financial advice. By making use of The Institutional Risk Analyst web site and content, the recipient thereof acknowledges and agrees to our copyright and the matters set forth below in this disclaimer. Whalen Global Advisors LLC makes no representation or warranty (express or implied) regarding the adequacy, accuracy or completeness of any information in The Institutional Risk Analyst. Information contained herein is obtained from public and private sources deemed reliable. Any analysis or statements contained in The Institutional Risk Analyst are preliminary and are not intended to be complete, and such information is qualified in its entirety. Any opinions or estimates contained in The Institutional Risk Analyst represent the judgment of Whalen Global Advisors LLC at this time, and is subject to change without notice. The Institutional Risk Analyst is not an offer to sell, or a solicitation of an offer to buy, any securities or instruments named or described herein. The Institutional Risk Analyst is not intended to provide, and must not be relied on for, accounting, legal, regulatory, tax, business, financial or related advice or investment recommendations. Whalen Global Advisors LLC is not acting as fiduciary or advisor with respect to the information contained herein. You must consult with your own advisors as to the legal, regulatory, tax, business, financial, investment and other aspects of the subjects addressed in The Institutional Risk Analyst. Interested parties are advised to contact Whalen Global Advisors LLC for more information.

Comments