Large Financials Slide in WGA Bank Top 100; Trump on Affordability? Really?

- Feb 1

- 8 min read

February 2, 2026 | Over the past several months, we have described to readers of The Institutional Risk Analyst the steady retreat of large-cap bank stocks we track in the WGA Bank Top 100. Suffice to say that large US banks are now in full retreat and they have a lot of company with independent mortgage banks (IMBs) likewise getting shellacked. As Q1 earnings roll in for the remaining public filers, it only gets better from here.

For subscribers to the Premium Service of The IRA, we provide a summary of our bank test results on the IRA website. The WGA Bank Top 100 test group is subjected to five measures focused on market returns and fundamentals. Of note, the average deviation between test subjects widened very dramatically since Q4 2025, indicating much higher variability and lower consistency in the group. A number of smaller bank stocks have risen in the rankings, but mostly because the larger cap names are falling faster. Consider some striking examples:

American Express (AXP) ranked #1 in Q4 2025, but fell to 11th in the latest WGA Bank Top 50 ranking because of poor market performance.

Goldman Sachs (GS) ranked 11th in Q4 2025 but has risen to #1 thanks to strong earnings and market performance.

Morgan Stanley (MS) maintained its position at #3 in Q1 2026, but Northern Trust (NTRS) rose from 13th to 2nd. Again, other names fell away.

SoFi Technologies (SOFI) was #2 in Q4 2025 and is another example of a leader in 2025 that has fallen back, in this case to 39th in Q1 2026.

JPMorgan (JPM) ranked 5th in Q4 2025, but has fallen to 41st because of poor market performance. What does it suggest when JPM retreats so rapidly to the middle of the group?

There continues to be an enormous amount of churn in the top 50 banks. Goldman Sachs and Citigroup (C) are the only two large institutions in the top 25 this quarter. Citi dropped from 16th in Q4 2025 to 25th in Q1 2026.

Names like tiny Lending Club (LC), which led the bank group in the second half of 2025, have since fallen back due to concerns about soft Q1 2026 guidance, concerns over core EPS missing expectations, and high share price volatility.

The fact that the Federal Open Market Committee is unlikely to cut interest rates in 2026 is another factor weighing on bank stocks. In a recent commentary (“The Martyrdom of Jerome Powell”), we noted that Fed Chairman Jerome Powell may remain on the Fed’s Board of Governors through the end of his term in January 2028.

The addition of Kevin Warsh as Fed Chairman does not change the ST calculus on the FOMC in terms of support for further rate cuts. Even as a former Governor, Warsh begins his term as leader of a minority on the Committee, especially if former Chairman Powell remains on the Board. This is why the inability of Trump to blame Powell for the astronomical increase in home prices, as we discuss below, is so remarkable.

More importantly, banks and nonbanks alike are entering a period of increased uncertainty in terms of earnings and rising credit costs. Last month we published a comment on the risks to banks from loans to private equity funds (“Does Private Credit Hurt Bank Stocks?”). The latest Treasury refunding of a mere three quarters of a trillion dollars illustrates why that the bias in LT yields and residential mortgage rates is higher in 2026, yet this factor is never discussed.

There is an enormous amount of forbearance by large banks with respect to defaulted loans to private equity firms and other non-bank financial institutions (NBFIs). As we've noted previously, principal paid in kind on original principal or "POOP" is a default by any other name. The amount of fraud and concealment involved in private equity loans is equally large. Larger bank stocks are retreating in 2026 because savvy investors suspect that bad news is coming on the commercial side of the ledger.

The stated default rates across most banks remained low in Q4, but we suspect that will not be the case for much longer. Even though ST interest rates have fallen in the past year, the festering credit problems in private equity and credit, and commercial real estate, are likely to be in the headlines for banks through 2026. But the big risk headed for US markets in 2028 is a maxi correction in home prices. Remember, misery on the 8s.

Subscribers to the Premium Service of The Institutional Risk Analyst may view the latest WGA Bank Top 50 results by logging into the website. An Excel copy of the entire 100 bank test group of bank holding companies and unitary banks is also provided.

Mortgages and Affordability

President Donald Trump said during a press conference last week that his administration will keep home values high while expanding ownership, arguing rising prices build household wealth. This is a remarkable statement, yet nobody in the big media challenged his assumptions. With the Treasury raising trillions in new debt in 2026, exactly how do mortgage rates fall? In fact, the reality in the market is just the opposite.

High home prices caused by the Powell FOMC have masked the cost of default even while shielding the government and investors from the cost, but this is hardly a normal state of affairs. High home prices have hidden the financial cost of default, but politically the top agenda item is "affordability" due to the Fed's massive inflation of home prices. As the cost of credit again reappears, valuations for banks and nonbanks alike will suffer.

When you see that loss given default on large prime bank mortgage loans is still ~ zero, but delinquency on FHA loans is at 11% and climbing, that tells you that home prices generally are headed for an eventual and substantial correction. Insiders in the mortgage industry are anticipating a tough year ahead and further forced consolidation in an industry that still cannot manage to make consistent profits even with mortgage rates near 6%.

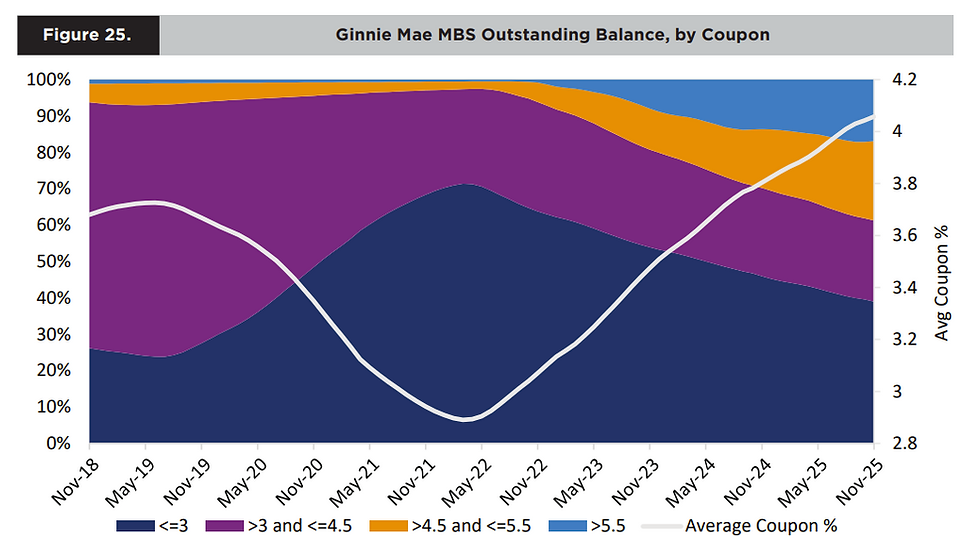

Remember that high home prices subsidize the cost of default, even on the risky FHA/VA/USDA market served by Ginnie Mae. But low average coupons left over from COVID for the $14 trillion in 1-4 family mortgages locks in half of all assets from the market. The chart below shows the distribution of coupons in the $3 trillion Ginnie Mae market from that agency's excellent Global Market Analysis report.

The good news is that mortgage rates have fallen 1% in the past year. The bad news is that the average residential mortgage coupon in the industry is just barely above 4%. Even though mortgage rates have fallen a point to ~ 6.25% today, home prices remain 10-20% too high in most markets for new home buyers to make up a significant portion of volumes. And those older northeast millennials sitting happy in the winter cold with 3% mortgages have no reason to sell.

Eventually Congress will be forced to waive capital gains taxes on residential homes to spur sales and free up supply. As a result of the "lock-in" effect of ultra low interest rates, refinance volumes are rising much faster than volumes for purchase loans and that trend is likely to continue, thwarting election years stunts to help affordability. Even if the Warsh-led FOMC were to push short-term interest rates down into the 2s, home prices are still too high in terms of affordability.

Does President Trump understand this conundrum? Probably not nor does Trump's team seem to appreciate the true reason that Chairman Powell should resign, namely excessively high home prices caused by too much for too long by the Yelln/Powell FOMCs. How is it that President Trump's communications team could not hang the burning tire of home price affordability around the neck of Jerome Powell?

“I don’t want those values to come down,” said Trump absurdly, referring to high home prices. “We have millions of people that own houses and, for the first time in their life, they’re wealthy because the house is worth $500,000 or $600,000 or more or less, but more money than it’s ever been worth before. I don’t want to do anything to knock that down.” The national pastime in America, after all, is inflation.

Source: FDIC/WGA LLC

The familiar chart above shows net losses by banks on prime residential mortgage loans near zero, another way of saying that home prices are way too high. The 50-year average net loss on bank owned 1-4s, excluding the period of COVID, is around 70% of the loan amount.

Notice in that same charts that the loss rate on relatively prime bank multifamily loans is near 100%, an illustration of the vast amounts of fraud in commercial lending. A 2026 FHFA OIG report detailed a 2023–2024 spike in multifamily fraud, with open investigations rising from 14 to 193. Fannie Mae adjusted its allowance for loan losses by over $400 million, driven by fraud in loans originated between 2020 and 2023. We suspect that credit expenses for both GSEs due to fraud in multifamily loans will increase.

The true crime of the Yellen/Powell FOMCs was forcing down the cost of default in 1-4 family loans to less than zero by expanding the Fed's balance sheet grotesquely. The Fed's reckless experiment with the US economy not only pushed up home prices, but enabled a period of fraud and speculation that is now in process of collapsing upon itself. Yet incredibly, the Trump White House is incapable of articulating this issue in public.

More, Chairman-nominee Kevin Warsh has a problem if he really, really thinks that he can reduce the Fed's balance sheet significantly from currently levels. Indeed, further rate cuts by the Fed may push LT interest rates higher, killing any benefit for lenders or home owners. We suspect that the Fed will be forced to increase bond purchases before too long, another reasons that investors are running out of financials. The chart below from FRED shows the Fed's system open market account (SOMA).

Just as banks and many other sectors of the stock market are likely to give back the supranormal gains of 2025, the 50% appreciation of home prices since 2020 also is long overdue for a correction. Read our biography of Stan Middleman who made the call on "Misery on the 8s" years ago.

In the next Premium Service edition of The Institutional Risk Analyst, we’ll be reviewing the results for PennyMac Financial (PFSI) and talking about the outlook for the mortgage sector in 2026. As a longtime reader of The IRA who works in the bowels of the mortgage industry wrote to us:

"After reading a bunch of stuff from street analysts, it seems that PFSI’s earnings miss caught them by surprise. The miss was very significant, and combined with their forward guidance, a very negative representation of prospects for the industry. Street consensus for EPS was $3.23 but came in at $1.97, a 39% miss. Revenue came in $101mm below consensus a 16% miss."

The Institutional Risk Analyst (ISSN 2692-1812) is published by Whalen Global Advisors LLC and is provided for general informational purposes only and is not intended for trading purposes or financial advice. By making use of The Institutional Risk Analyst web site and content, the recipient thereof acknowledges and agrees to our copyright and the matters set forth below in this disclaimer. Whalen Global Advisors LLC makes no representation or warranty (express or implied) regarding the adequacy, accuracy or completeness of any information in The Institutional Risk Analyst. Information contained herein is obtained from public and private sources deemed reliable. Any analysis or statements contained in The Institutional Risk Analyst are preliminary and are not intended to be complete, and such information is qualified in its entirety. Any opinions or estimates contained in The Institutional Risk Analyst represent the judgment of Whalen Global Advisors LLC at this time, and is subject to change without notice. The Institutional Risk Analyst is not an offer to sell, or a solicitation of an offer to buy, any securities or instruments named or described herein. The Institutional Risk Analyst is not intended to provide, and must not be relied on for, accounting, legal, regulatory, tax, business, financial or related advice or investment recommendations. Whalen Global Advisors LLC is not acting as fiduciary or advisor with respect to the information contained herein. You must consult with your own advisors as to the legal, regulatory, tax, business, financial, investment and other aspects of the subjects addressed in The Institutional Risk Analyst. Interested parties are advised to contact Whalen Global Advisors LLC for more information.

Comments