What Does a Smaller Fed Balance Sheet Mean for Inflation & Interest Rates?

- May 17

- 7 min read

Updated: May 18

May 18, 2026 | Back in September of last year (“Trading Points: Klarna & Figure IPOs”) , we wrote critically of Klarna Group plc (KLAR) prior to its IPO:

“Our basic view of Klarna is that the offering is a leading example of damaged goods c/o PE firms. The firm’s $14 billion offering price marks a steep decline from the $45.6 billion valuation assumed in 2021, when Japan’s SoftBank made a $639 million investment.”

Since the IPO, KLAR has lost more than 60% of its value vs an 18% gain for the NASDAQ composite. As of Friday’s close, KLAR has a market capitalization of just over $5 billion or about 1/10th of the private valuation in 2021. The Klarna transaction illustrates the basic problem with private equity and credit, namely that the sponsors and insiders have no incentive to be truthful in their statements to investors.

A colleague in the media asked the other day how private investment strategies had grown so large. The short answer is inflation. Asset prices have steadily increased since 2008, in large part because the Fed has refused to allow deflation and, indeed, has encouraged inflation to prevent the US financial system from seizing up. As we wrote in the book “Inflated: Money, Debt and the American Dream”:

“The vast amount of debt incurred by governments around the world has forced policymakers to err on the side of ample liquidity in fact, regardless of what the official statements say about encouraging jobs and fighting inflation. In the fall of 2024 on the eve of a presidential election, the Fed decided to end the battle against inflation a little early, a remarkable development given that the central bank had barely reduced the level of bank reserves and home prices had not fallen. Yet the fact was that the Fed was unwilling to reduce market liquidity for fear of causing another systemic event in the bond market a la December 2018 or March 2020.”

So long as the general level of asset prices rose, the private equity and credit markets seemed attractive. The systemic bias of the public equity markets to rise due to the predominance of passive strategies contributed to this pleasing illusion. Asset price inflation made the cost of credit negative in residential real estate, encouraging growth in credit strategies. But would investors of all stripes be pouring new cash into private equity or credit strategies if public equity valuations or home prices were flat or even falling?

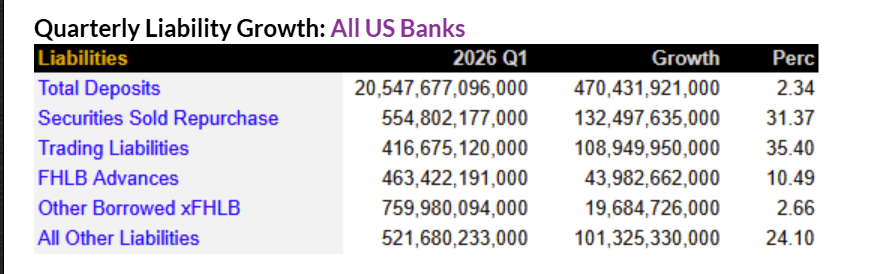

Ponder another example of systemic inflation. The assets of the US banking system “grew an astonishing $888.03 Billion (3.52%) to finish the 1st Quarter at $26.145 Trillion,” notes Bill Moreland of BankRegData. What drove this remarkable increase? Growth in the federal debt, deposits and also in bank loans. "This is a simply stunning number and the natural question is: where did all the funding come from?" Moreland asks. The table below shows the growth rates in bank liabilities in Q1 2026 which support this asset growth.

Source: FDIC/BankRegData

Most economists will tell you that the federal debt is not inflationary and that the size of bank reserves does not impact asset prices. Modest amounts of federal debt is not inherently inflationary, but deficit spending that creates the debt does contribute to overall demand and thus asset inflation. Also, the debt issued by Treasury fuels more borrowing. When bank assets grow by 3.5% in a single quarter, that inflates asset prices directly and indirectly.

When the government borrows money to inject high levels of demand into a supply-constrained economy, as in 2020 during COVID, it drove up prices for housing. The fact that the Fed drove interest rates down to zero only added to the inflationary impact of huge fiscal action, an effect that continues to push up prices even today. As the Budget Lab at Yale University notes in a 2025 paper:

“Higher debt adds to the risk of inflationary pressure in both the short- and the long-run, through aggregate demand, inflation expectations, crowding-out of private investment, and worries about fiscal dominance.”

A Shrinking Fed Balance Sheet?

Fed Chairman Kevin Warsh has made reducing the size of the central bank’s balance sheet and thus the level of bank reserves a priority. Most mainstream economists, of course, don’t think that the size or composition of the Fed’s balance sheet matters.

In fact, the Fed’s purchase of securities from 2020 onward (and the sequestration of massive duration inside the system open market account or "SOMA") actually allowed the FOMC to keep ST interest rates higher for longer. The chart below shows the SOMA with the red line representing Treasury debt and the green line mortgage securities.

If the Fed had not gone overboard with QE during and after COVID, the private markets would have needed to support trillions in Treasury and mortgage securities, and the FOMC would have needed to keep the target for federal funds lower to compensate for the additional duration held by the private markets. When the Fed buys Treasury debt, it is the economic equivalent of giving a sick patient morphine.

If the Warsh Board of Governors (not the FOMC note) decides to move forward with a smaller Fed balance sheet, how the Treasury responds will be crucially important, notes Bill Nelson at Bank Policy Institute. In his must-read May 8th missive, Nelson lays out three scenarios for a shrinking Fed balance sheet, which would result in a commensurate decline in bank deposits.

The most likely of the three Nelson scenarios is that the Fed shrinks the SOMA and Treasury issues zero duration T-bills in response, meaning that the FOMC would not need to lower ST rates.

“Suppose instead the Treasury replaced the Fed’s portfolio holdings with new debt that had the same 5-year duration as the existing public debt, Nelson writes. “In that case the committee would need to reduce the target by 62 bp to leave the policy stance unchanged.”

The more interesting possibility for Warsh involves a swap of the $2 trillion in MBS in the SOMA, which has a duration that is 3x the Fed’s whole portfolio. If the Treasury were to swap the Fed for the MBS with say 7-10 year notes, the monetary impact would be neutral. Then comes the bigger question of what to do with the MBS outside the duration sequestration of the Fed’s balance sheet?

As we’ve written before ("Should the FOMC End Fed Funds Targeting? Issue CMOs?"), the obvious answer to the problem of the Fed's MBS position is for Treasury to hold the agency and government MBS. The White House can then direct the GSEs, Fannie Mae, Freddie Mac and Ginnie Mae, to engage with Street dealers and large end investors to restructure the paper into collateralized mortgage obligations (CMOs). The idea is to place this attractive, “AAA” paper with banks, insurers and pensions, forever.

Insurers in particular would be natural buyers of the long-duration tails from these deals. Even though the paper would technically be “held by the public,” the fact of the duration transformation of the different CMO tranches would render the issuance neutral in terms of the public markets and FOMC policy. Warsh can correct the grievous error of QE under Ben Bernanke, Janet Yellen and Jerome Powell of doing too much for too long, and without creating yet another problem for policy.

Chairman Warsh argue that the reduction in the size of the SOMA warranted a permanent reduction in the federal funds market. More, the permanent interment of the $2 trillion in duration represented by the Fed’s MBS hoard would give the Committee some additional flexibility in terms of managing the duration of the Treasury’s public market.

“According to the New York Fed Market Group’s Annual Report, the duration of the Fed’s Treasury portfolio at the end of last year was 6.7 years,” Nelson wrote, but the true duration of the $2 trillion in MBS in the SOMA today is closer to 16-20 years. When these MBS held by the Fed were created during COVID, the duration was closer to 2-3 years.

Source: dataQollab

The good news is that Warsh can credibly advocate a cut in the ST target for Fed funds, but it involves shrinking the Fed balance sheet and reserves by $2-3 trillion and some artful coordination with the Treasury in the process. Given Nelson’s views, the best route may be for Treasury to issue longer term, longer duration debt, which would arguably force a 50bp rate cut by the Committee in response.

We all need to remember that shrinking the Treasury portion of the Fed balance sheet is the easy part. The $2 trillion in notional amount of MBS held in SOMA, which now has an effective duration that is much, much bigger than the rest of the portfolio combined, requires some subtlety. The good news is that the agencies and Ginnie Mae are thinking about a potential Fed MBS swap with Treasury. Wall Street can make it all happen and profit handsomely by selling a lot of “AAA” rated CMOs.

The Institutional Risk Analyst (ISSN 2692-1812) is published by Whalen Global Advisors LLC and is provided for general informational purposes only and is not intended for trading purposes or financial advice. By making use of The Institutional Risk Analyst web site and content, the recipient thereof acknowledges and agrees to our copyright and the matters set forth below in this disclaimer. Whalen Global Advisors LLC makes no representation or warranty (express or implied) regarding the adequacy, accuracy or completeness of any information in The Institutional Risk Analyst. Information contained herein is obtained from public and private sources deemed reliable. Any analysis or statements contained in The Institutional Risk Analyst are preliminary and are not intended to be complete, and such information is qualified in its entirety. Any opinions or estimates contained in The Institutional Risk Analyst represent the judgment of Whalen Global Advisors LLC at this time, and is subject to change without notice. The Institutional Risk Analyst is not an offer to sell, or a solicitation of an offer to buy, any securities or instruments named or described herein. The Institutional Risk Analyst is not intended to provide, and must not be relied on for, accounting, legal, regulatory, tax, business, financial or related advice or investment recommendations. Whalen Global Advisors LLC is not acting as fiduciary or advisor with respect to the information contained herein. You must consult with your own advisors as to the legal, regulatory, tax, business, financial, investment and other aspects of the subjects addressed in The Institutional Risk Analyst. Interested parties are advised to contact Whalen Global Advisors LLC for more information.

Comments