The Wrap: AI and Metals Surge, Dollar Gyrates and Private Credit Sinks

- May 7

- 5 min read

In this week’s edition of “The Wrap,” we feature our view of the top events in Washington and on Wall Street over the past week. And do watch “The Wrap with Chris Whalen” on The Julia LaRoche Show every Saturday on YouTube to catch our discussion of what’s hot and what’s not in the world of finance and investing. Below for subscribers to our Premium Service we have instructions how to access a replay of last week's quarterly call.

May 8, 2026 | As the week came to an end, reports of a possible peace deal with Iran pushed up gold prices and hurt the dollar. Is a peace deal for real? President Donald Trump has on numerous occasions indicated that a deal is near, Bloomberg reports, though none has materialized. What is under discussion as this week ends is a month-long cease fire -- maybe. As this issue of The Wrap was being posted, the US and Iran had resumed hostilities.

We remain skeptical that the government of Iran will agree to a cessation of hostilities with Israel and the US, especially while the government of Benjamin Netanyahu continues its campaign of ethnic cleansing in Gaza and Lebanon. Even if the US somehow manages to craft a peace deal with Iran, Israel's increasingly authoritarian government must continue the policy of continuous war or lose its grip on power. Will Israel hold elections as scheduled this fall?

Rumors of a deal in the Middle East eased inflation worries, at least for now, but the reality is the much of Asia, Europe and event the US are facing shortages of fuel and key industrial products as a result of the Iran war. But shortages are also good for prices. Easing tensions reduced the demand for the dollar as a safe-haven asset, allowing it to fall on both Wednesday and Thursday this week.

Gold and Silver Surge

In the past five trading days, gold has moved up almost 3% but silver has done even better. Physical supply constraints in India and Asia are pushing prices for gold and silver higher, illustrating the disconnect between the momentum driven financial markets in the US and Europe and the physical market in Asia.

Source: Google Finance (5/7/26)

Indian banks face an unprecedented five-week halt in gold and silver imports, causing domestic prices to surge and threatening shortages, reports The Economic Times. Administrative hurdles and tax uncertainties have stalled shipments since April 1st.

“Roughly 70% of global silver comes as a byproduct of base‑metal mining,” writes Silver Academy, “making dedicated primary silver producers the cleanest way to capture upside from a tightening physical market.” We continue to add to our positions in both gold and silver.

We have updated the WGA Precious Metals Top 25 list for subscribers to our Premium Service. The top performer of the group remains the ZKB Silver ETF (0VR6.L). We now have 47 funds and mining stocks in our Precious Metals group, which provides our subscribers with a broad range of ways to get exposure to the metals sector.

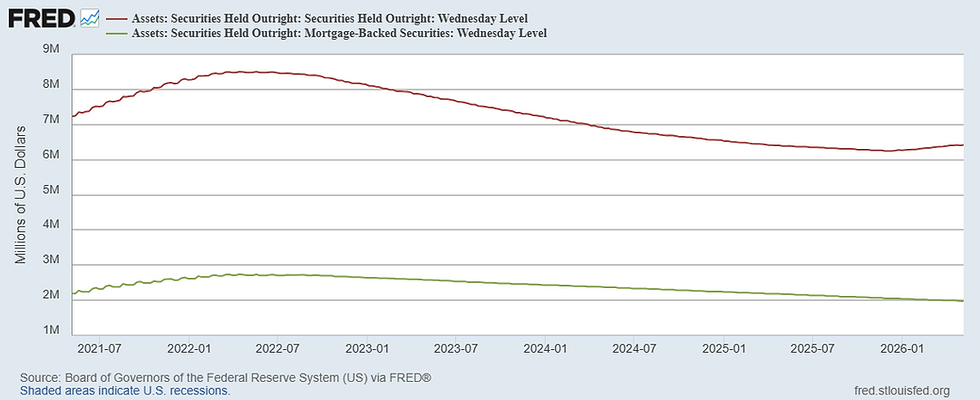

Fed Balance Sheet Grows

We’ve noted in past comment that Kevin Warsh, the nominee to become the next chairman of the Federal Reserve Board, wants to shrink the balance sheet of the central bank, but in fact the Fed’s balance sheet is growing. Some economists think that setting the level of reserves is a policy choice, but we believe instead that the size of the Fed’s balance sheet is linked to the growth in public debt. Our view is seasoned by years of working in Mexico.

The Federal recently resumed growing its balance sheet, with total assets rising to approximately $6.63–$6.7 trillion as of early May 2026. After peaking near $9 trillion in 2022 and subsequently shrinking, the Fed began increasing holdings to add reserves, including a $42 billion rise in February 2026, comprised mostly of T-bills. Purchases of debt for the system open market account is inflationary since it increases the level of bank deposits and assets.

Private credit continues to be a source of concern Black Rock’s (BLK) sponsored TCP Capital (TCPC) cut the value of its publicly-traded private credit fund by about 5%, due to troubled loans, markdowns and lower returns. And Apollo Global (APO) CEO Marc Rowan says that he plans to offer investors daily faux valuations for private credit funds by the end of September, a move that they hope will ease worries about the health of an opaque world of private lending. But do investors even care?

Meanwhile, the AI sector in stocks has once again surged as earnings results for a variety of players have come in strongly. Our LT position in Advanced Micro Devices (AMD) is up 300% in the past year. Nvidia (NVDA) also continued its strong performance, but is “only” up 80% in the past year. Micron Technology (MU) and energy infrastructure platform Hut 8 Corp (HUT) also stand out as top-performing AI-related stocks over the past week.

Subscribers to The IRA Premium Service may login and download a replay of last week's quarterly call on the Top Rankings page.

Recent Posts

WGA Bank Top 50 Q2 2026 | Bank Failures and Mortgage Bankers

Trading Points: China, Sulfur & Silver 银

The Institutional Risk Analyst (ISSN 2692-1812) is published by Whalen Global Advisors LLC and is provided for general informational purposes only and is not intended for trading purposes or financial advice. By making use of The Institutional Risk Analyst web site and content, the recipient thereof acknowledges and agrees to our copyright and the matters set forth below in this disclaimer. Whalen Global Advisors LLC makes no representation or warranty (express or implied) regarding the adequacy, accuracy or completeness of any information in The Institutional Risk Analyst. Information contained herein is obtained from public and private sources deemed reliable. Any analysis or statements contained in The Institutional Risk Analyst are preliminary and are not intended to be complete, and such information is qualified in its entirety. Any opinions or estimates contained in The Institutional Risk Analyst represent the judgment of Whalen Global Advisors LLC at this time, and is subject to change without notice. The Institutional Risk Analyst is not an offer to sell, or a solicitation of an offer to buy, any securities or instruments named or described herein. The Institutional Risk Analyst is not intended to provide, and must not be relied on for, accounting, legal, regulatory, tax, business, financial or related advice or investment recommendations. Whalen Global Advisors LLC is not acting as fiduciary or advisor with respect to the information contained herein. You must consult with your own advisors as to the legal, regulatory, tax, business, financial, investment and other aspects of the subjects addressed in The Institutional Risk Analyst. Interested parties are advised to contact Whalen Global Advisors LLC for more information.

Comments