SoftBank as Systemic Event; Update: Charles Schwab & Co

- Sep 27, 2023

- 9 min read

September 27, 2023 | Premium Service | In this issue of The Institutional Risk Analyst, we return to Charles Schwab & Co (SCHW), a name that figures near the top of our subscriber emails and the “short-list” for many equity traders. Before we delve into the increasingly problematic world of US banks, however, let’s take note of the latest machinations from SoftBank Corp, the profoundly idiosyncratic Japanese hedge fund guided by the equally unpredictable Masayoshi Son.

SoftBank Corp claims that it will attempt to raise up to 120 billion yen ($808.79 million) via Japan's first public offering of bond-type class shares, Bloomberg News reports. Son, of note, owes SoftBank $5 billion which he “borrowed” to boost his compensation after a year of record losses. The latest developments come in the wake of the dismal performance of two SoftBank equity offerings for Better Holdings (BETR) and ARM Holdings (ARM).

Online lender BETR merged with a SPAC f/k/a Aurora on August 23, 2023 and initially traded at $17 per share, but subsequently collapsed to under $1. Today BETR is trading at $0.50 and has been placed on a “death watch” by several mortgage publications. Like many mortgage companies with the misfortune to be public, BETR is suffering a “valuation reset.”

Meanwhile, the “blockbuster” ARM IPO is likewise starting to feel the strong gravitational pull of rising interest rates and a slowing global economy. The much-anticipated offering of a small stake in ARM came after SoftBank’s failed attempt to sell the company to Nvidia (NVDA). The stock traded as high as $69 per share, but fell down into the mid-$40s on strong selling pressure before rebounding yesterday to close below the IPO price.

The poor performance of these two public offerings apparently caused the management of SoftBank to become unglued. SoftBank’s finance chief, Yoshimitsu Goto, lashed out at S&P after the rating agency refused to immediately upgrade the firm’s “BB” junk debt rating from S&P. Somebody needs to whisper in Mr. Goto’s ear that US rating agencies like "smooth transitions," something that SoftBank is obviously not going to provide.

Goto told the Financial Times he was “deeply disappointed” with S&P’s decision to stop short of an upgrade, despite raising its credit outlook from stable to positive. He went on yowling like a wounded hound and accused S&P Global of “not trusting the management.” True. Of note, SoftBank has "A" ratings from several non-US agencies.

Just for the record, Mr. Goto, most reasonable people don’t trust SoftBank management because of the firm’s very apparent lack of internal systems and controls. We also find it interesting that SoftBank is seeking to raise capital via a debt offering after a series of missteps and market disappointments. Has the equity tap run dry, Mr. Son?

As “Big in Japan” noted in a comment to the Financial Times: “A finance director who can’t hold his nerves is probably dealing with a very unsustainable financial situation…And yes we don’t believe SoftBank financial discipline or investment policy. The evidence is written all over the wall!” Again, very true.

So much of the image of success used by SoftBank to raise billions in private equity in past years was predicated on the illusion of value in a zero-interest rate environment. In today’s market, however, we think risk managers and investors ought to ask themselves whether the public behavior of Softbank’s executives deserves to be met with confidence or terror.

The public behavior and decision-making processes of SoftBank suggest that the organization is in trouble. The choice to move forward with the BETR IPO, for example, oozes of desperation and may create legal liability for SoftBank. It’s not clear whether Son or Goto or their other colleagues care. A year from now, will we be speaking about SoftBank and Masayoshi Son in the past tense?

“[BETR’s] SPAC partner, Aurora Acquisition Corp., once traded as high as $62.91 a share,” notes Paul Muolo of Inside Mortgage Finance. “Might a reverse stock split be in order at some point?”. Maybe. Do you think that the Financial Stability Oversight Council discussed SoftBank last week? Probably not.

Charles Schwab & Co

Back in March of 2023, as the proverbial wheels were falling off the cart in banks, Charles Schwab (SCHW) fell off the edge of the table, dropping from ~ $80 per share down to the mid-50s. We mentioned this fall from grace with respect to both SCHW and Citigroup (C), which has been wallowing at 0.4x book value since COVID.

Is the 30% downward price adjustment in SCHW due to some structural problem with the bank or simply reflects less air in the valuations for all banks? Or was the runup in the stock from 2021 simply a bubble? We suspect the latter is the case. Note that looking back over the past five years, SCHW is actually up 10% even today.

Source: Google Finance

The first question to ask is the Street’s posture on the stock. Short-interest has been trending lower since mid-year, but was never more than 30 million shares vs a 10 million share per day average. SCHW has a $100 billion market cap at the close on Tuesday or a price/book of around 3.5x vs over 5x pre-March ‘23. Despite some vociferous critics, SCHW does not seem to be distressed at present. But that stability may be temporary thanks to the FOMC

The Street, needless to say, has “buy” and “strong buy” ratings on SCHW, but these recommendations may be tough to fulfill given the rising questions about banks in the minds of investors. Earlier we discussed how names like SCHW and Citigroup (C) have experienced significant declines in valuation, but obviously the former has been merely marked down to “only” 3.5x book value while Citi has been trading below 0.5x book for several years.

If we compare SCHW with the other asset gatherers in our surveillance group, the picture is considerably better than the market performance suggests. The big question we are pondering is whether SCHW and other names are starting to spread out again in terms of valuation after a five-year roller coaster ride c/o the FOMC. We include Goldman Sachs (GS), Morgan Stanley (MS), Raymond James (RJF) and Stifel Financial (SF).

First, we look at credit performance and SCHW and SF are in competition for the lowest net-loss rate. SF has actually reported zero credit losses for several quarters, while SCHW has a loss rate that is slightly above zero. The rest of the group are normalizing their credit profiles, but losses remain very low with the notable exception of Goldman Sachs. GS at 62bp of net loss is 2x Bank of America (BAC) and just behind Citi.

Remember, we are talking net credit losses as a percentage of average assets. GS has a much smaller credit book than other commercial banks, thus our concern. We noted earlier that even with the sale of Marcus loan assets, the credit performance of GS is still festering. What is going on?

Source: FFIEC

Notice that the net credit losses for GS have almost returned to 2020 levels, again begging the question as to why the bank is reporting such anomalous results in credit. SCHW, by comparison, reported 1bp of net loss in Q2 2023. Most of the other asset gatherers have low credit loss rates that are also stable.

Next on the agenda is the gross spread on loans and leases, a measure of how the bank prices risk. The spread also gives you an idea of the sort of customer that the bank is pursuing in its business operations. As the chart below suggests, most of the group has repriced their portfolios to about 6% gross spread, but GS is over 10%, suggesting that the target customer is decidedly subprime. The spread also suggests that GS is under significant pressure in terms of funding, as we’ll discuss below.

Source: FFIEC

Notice that SCHW and SF have the lowest gross loan spreads in the group, which reflects their lower funding costs and also a less aggressive stance in the market. In terms of unused credit that may be drawn, SCHW has less than $2 billion in the unused portions of HELOC commitments that are fee paid or otherwise legally binding and not much else.

GS, on the other hand, has $69 billion in unused credit card lines, $2.5 billion in commitments for construction loans, $125 billion in unused commercial & industrial and other commercial credit lines, and another $6 billion in standby letters of credit. In terms of exposure at default, a Basel I measure of vulnerability to market turns, GS leads the pack but SCHW is at the bottom of the list. The two business models could not be more different.

Net loans & leases at SCHW was only 20% of total assets at Q2 2023, with 50% of total assets in debt securities and mutual funds. GS had only 14% of total assets in loans, 40% in deposits and federal funds sold, and the remainder in trading assets. GS reported negative $3.2 billion in accumulated other comprehensive income (AOCI) at Q2 2023 while SCHW reported -$20 billion in AOCI at Q2 2023.

The fact that GS does not hold securities for investment is a major advantage for the firm and somewhat offsets the outsized market and credit risk taken by the firm. Bloomberg reports that the average price of all fixed income securities in the US is 86 cents on the dollar, meaning that many banks and other intermediaries are insolvent now. If the FOMC makes another quarter-point rate hike, the average will fall towards 80 and GNMA 3s will be trading in the mid-70s vs par.

For SCHW, bonds is a big pain point because its half of the balance sheet and also because in capital terms, the Treasury, GNMA and agency MBS has zero or low (20%) risk weights for Basel purposes. The chart below shows the swings in SCHW AAOCI Since 2020. Half of the bank’s $38 billion in equity is impaired as of Q2 2023 and we expect this capital impairment to grow.

Source: FFIEC

In response to these changes, the management of SCHW has taken significant steps to change the composition and funding of its balance sheet. As we predicted in an earlier note, SCHW has decreased the assets of the bank 20% since 2021 and deposits by over 40% in the past year alone. The bank substituted debt for the deposit runoff, allowing management to control the duration of the book. Brokered deposits and short-term debt have grown significantly.

SCHW is below $500 billion in assets as of Q2 and we’d not be surprised to see further significant runoff. The shift in funding and other changes are clearly one major factor behind the drop in valuation. Yet having said all of that, SCHW’s funding costs are tracking at the bottom of Peer Group 1, as shown in the chart below.

Source: FFIEC

Note that SCHW is trending at only about 60% of the funding cost for Peer Group 1 and the other banks in the group. GS has thankfully seen a decrease in the rate of change for its average funding costs. And MS has engineered a dramatic decrease in funding costs by dropping 80% of the bank’s more costly MMDAs and savings accounts. Of note, MS had only -$6 billion in AOCI vs $100 billion in equity capital in Q2 2023.

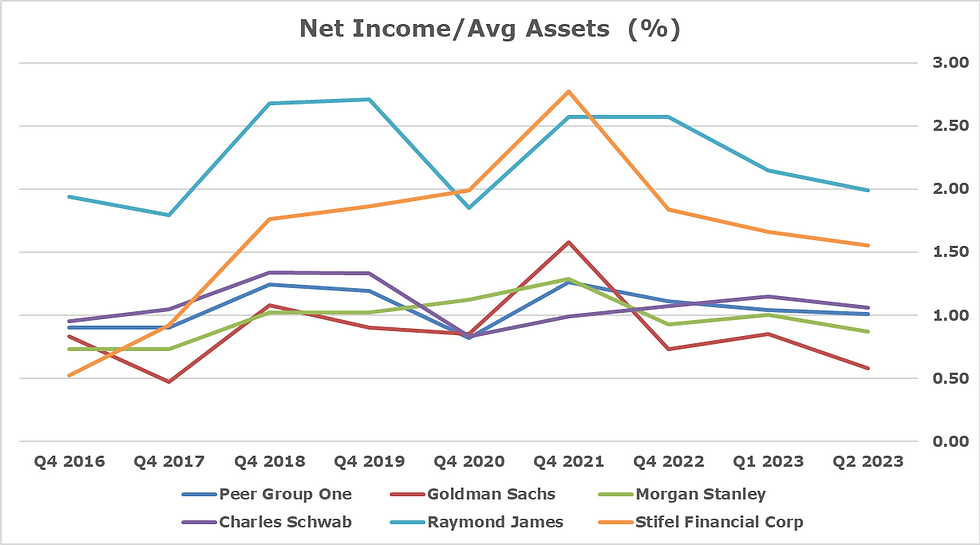

In terms of reported earnings, SCHW is in the middle of the herd, tracking Peer Group 1 and MS. RJF and SF are the best performers in the group measured against average assets, but the entire cohort of asset gatherers is headed lower as the Fed’s market operations squeeze net income. Notice that GS is in a nose dive, with next income to average assets half of Peer Group 1, but MS is trending lower as well.

Source: FFIEC

Bottom line on SCHW is that management is making significant changes in the business, dropping deposits and assets as the bank slowly unwinds its large fixed income position. While the bank's balance sheet is a source of fascination for short-sellers, its is the $8 trillion in assets under management that is the core of the business.

We expect SCHW to continue to shrink the bank, perhaps as low as $400 billion by year end. But in the meantime, we see no reason to go long the stock at this juncture and believe that the Sell Side "Buy" recommendations are misplaced. As the prospect of a further increase in interest rates looms, SCHW and other banks may come under renewed selling pressure as the year grinds to an end.

DISCLOSURE

The Institutional Risk Analyst (ISSN 2692-1812) is published by Whalen Global Advisors LLC and is provided for general informational purposes only and is not intended for trading purposes or financial advice. By making use of The Institutional Risk Analyst web site and content, the recipient thereof acknowledges and agrees to our copyright and the matters set forth below in this disclaimer. Whalen Global Advisors LLC makes no representation or warranty (express or implied) regarding the adequacy, accuracy or completeness of any information in The Institutional Risk Analyst. Information contained herein is obtained from public and private sources deemed reliable. Any analysis or statements contained in The Institutional Risk Analyst are preliminary and are not intended to be complete, and such information is qualified in its entirety. Any opinions or estimates contained in The Institutional Risk Analyst represent the judgment of Whalen Global Advisors LLC at this time, and is subject to change without notice. The Institutional Risk Analyst is not an offer to sell, or a solicitation of an offer to buy, any securities or instruments named or described herein. The Institutional Risk Analyst is not intended to provide, and must not be relied on for, accounting, legal, regulatory, tax, business, financial or related advice or investment recommendations. Whalen Global Advisors LLC is not acting as fiduciary or advisor with respect to the information contained herein. You must consult with your own advisors as to the legal, regulatory, tax, business, financial, investment and other aspects of the subjects addressed in The Institutional Risk Analyst. Interested parties are advised to contact Whalen Global Advisors LLC for more information.

Comments