Who is the Next Countrywide Financial? PennyMac, Rocket & UWMC

- May 10

- 9 min read

Updated: May 12

May 11, 2026 | Updated | This week The Institutional Risk Analyst looks at the nonbank mortgage sector as the prospect for lower interest rates is fading fast. On the one hand, a number of the larger issuers are continuing to thrive even in a difficult interest rate market. Second lien mortgages and non-agency jumbo loans are growing as a percentage of overall production volumes.

On the other hand, the aggressive behavior of some issuers is distorting pricing for loans in the secondary market and may be creating the circumstances for the next systemic “surprise” in the nonbank sector. To us, Exhibit A in the category of a potential nonbank default event is United Wholesale Mortgage (UWMC), aka “Countrywide II.” (* We have no positions in any of the issuers discussed below.)

Cross Country Wins Two Harbors

If you were watching the auction for the crippled Two Harbors (TWO) REIT, you might feel both sad and concerned. Sad because TWO has a $2.1 billion mortgage servicing right (MSR) that is going to trade for half of that value due to the $1.3 billion negative net worth of the REIT. But we are more concerned because, as Rich Swerbinsky wrote on LinkedIn, UWMC seems to need this deal very badly, but clearly cannot afford it.

Last week, leading retail lender Cross Country Mortgage (CCM) raised their cash bid for TWO to $12 per share, matching a revised offer from UWMC at $12 per share of TWO. But the UWMC offer seemed more like window dressing to us than a serious counter to the CCM all-cash proposal.

“The CCM transaction delivers a fixed price all-cash consideration to every TWO stockholder — automatically and without election — with committed financing, no financing contingency, and a clear path to close in the shortest time frame,” Two Harbors CEO Bill Greenberg noted. “Our Board unanimously recommends that stockholders vote FOR the proposed merger with CCM.”

Part of the problem is that UWMC’s stock is simply not attractive as an alternative to the cash offer from CCM. The default stock consideration under UWM’s offer was worth approximately $7.88 per TWO share based on UWMC’s May 7 closing price, TWO noted. All three of the largest mortgage issuers have sold off dramatically since the start of the year as expectations for lower interest rates have evaporated in the heat of the war with Iran.

Source: Google Finance (05/08/2026)

There are ~ 294 million UWMC shares out trading publicly below $4, which means the shares essentially have no collateral value and even less value as an acquisition currency. Insiders control 13% of the public float and institutional holders 66%. But insiders control another 1.3 billion shares "that may be issued to SFS Corp. or its transferees or assignees in connection with future Exchange Transactions," according to the 2025 UWMC 10-K.

The Up-C structure of UWMC, which isolates the operating business from public shareholders in a partnership, is decidedly unattractive to investors from a credit perspective. To us, the public stock has no real value, especially when we consider the net debt of the issuer after excluding the mortgage servicing rights (MSR).

As we've noted previously, when looking at an independent mortgage bank (IMB), unsecured debt and MSRs need to be roughly in balance. In an economic sense, the unsecured debt holders really own UWMC, yet the operating assets may be beyond reach of all public investors. But the problems with UWMC run far deeper than the current stock price and have to do with an unsustainable business model that is damaging the entire residential mortgage industry.

United Wholesale Mortgage: Countrywide Redux

The basic issue with the UWMC business model is they pay too much for loans in order to protect their dominant (40% plus) market share in wholesale lending. Rocket Companies (RKT) is second at less than 10% and PennyMac Financial (PFSI) is third around 5%, according to Inside Mortgage Finance. As a result, UWMC is the largest nonbank lender in the US.

When mortgage rates were falling early in Q1, you would see “UWMC partners “ quoting way below market rates like 4.5%, rates not even visible in the pricing engines of most lenders. These brokers quote below market rates and hope the market gets there, but UWMC has been "buying down" loan coupon rates for years.

For example, UWMC is currently offering free 1-0 lender-paid temporary rate buydowns on conventional and government purchase loans through June 30, 2026. This initiative, which reduces the borrower's interest rate by 1% for the first year, was launched to boost affordability for broker partners, but ensures a cash loss for UWMC.

It is not uncommon for borrowers to receive unsolicited text messages after closing a loan offering to refinance a mortgage immediately at a lower rate. UWMC brokers also reportedly ignore legal prohibitions on contacting the customers of other lenders, saying: “I see you just refinanced, what is the rate you got?“ This is completely illegal without an opt in by the borrower.

Two decades ago, another extremely aggressive lender, Countrywide Financial, utilized similar lending practices to boost volumes. Countrywide was a thrift that had meager core deposits and habitually overpaid for loans to hurt competitors, forcing down profits for the entire industry.

Under CEO Angelo Mozilo, Countrywide aimed for massive market share, pushing risky private label loans and using a "race to the bottom" policy to match any competitor's offering – precisely the same modus operandi as UWMC. Due to these aggressive practices and subsequent legal fallout, Countrywide was forced into an involuntary sale to warehouse lender Bank of America (BAC) in 2008.

As we noted in an earlier comment, none of the warehouse lender banks serving UWMC today would even think of buying the largest US nonbank lender. In terms of reported earnings, UWM reported a strong start to 2026 with $44.9 billion in 1Q 26 loan origination volume, a 9.5% dip from the $49.6 billion in 4Q25, but a significant 39% increase year-over-year from 1Q 2025. The quarter marked their second-best first quarter in company history on a GAAP basis, but beneath the surface the UWMC story is far more complicated.

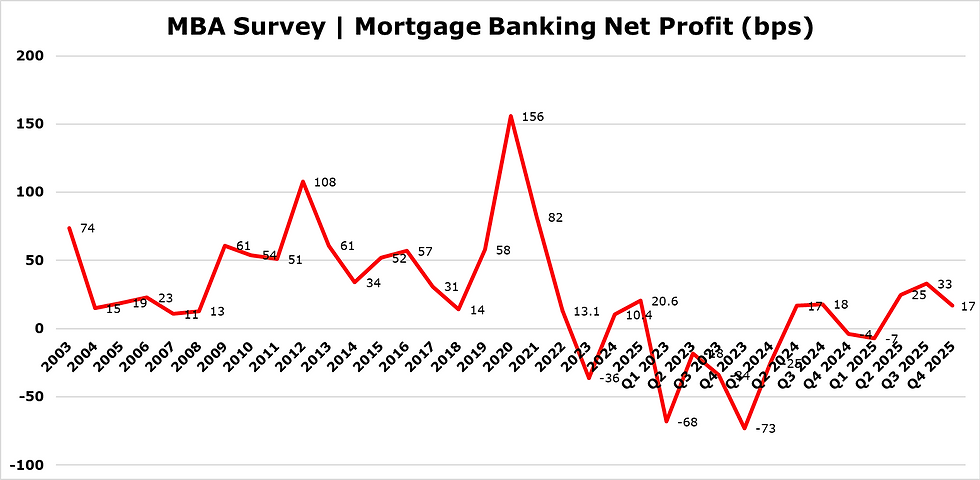

The willingness of UWMC to pay up for loans in order to gain market share has reportedly compressed gain-on-sale margins and profitability across the industry and saddled the company with excessive debt. Like Countrywide, we worry that UWMC is clearly overextended because of its aggressive business model and that this fact is hurting all of the public comps across the entire mortgage entire sector.

Source: MBA Quarterly Performance Report

Mat Ishbia, CEO of UWMC, said: “Q1 was an exceptional quarter for UWM and our second‑best first quarter of all time. The last time we delivered results of this magnitude, interest rates were nearly 50% lower, which underscores the strength, scale and resilience of our business. Our team and broker partners executed at the highest level, using UWM’s proprietary technology and AI‑powered tools like Mia to win more loans, more efficiently, every day.”

Winning more loans means, in simple terms, that UWMC is bleeding more cash. UWMC reported $450 million in liquidity in Q1 2026, but this is not nearly enough for a firm of their size. How does UWMC make up both the cash deficit and also the ugly GAAP disclosure? By selling mortgage servicing rights below cost, increasing corporate debt and adjusting the valuation of the firm’s MSRs to increasing borrowing capacity.

Creating conventional MSRs multiples above 6x cash flow, but selling them at or below 5x is not a great trade in our book. "In the past couple of years, they were also in the habit of selling long-duration low coupon MSR to fund the origination of low duration high coupon MSR," notes one industry insider maven. "My description of this was 'selling the gold to buy the lead' (and yes, a double-entendre on 'lead')."

Under GAAP, changes in the modelled fair value of the MSR flow through income in the same quarter. Thus while UWMC reported a decline in the size or unpaid principal balance (UPB) of its servicing book in Q1 2026, the valuation of the MSR magically increased by double digits, as shown in the table below.

United Wholesale Mortgage

Again, the UPB of the UWMC servicing book fell in Q1, yet the value of the related servicing asset magically went up double digits. Specifically, as of Q1 2026, UWMC apparently valued their combined MSR book at over 5.5x annual cash flows, an adjustment that accounted for most of their GAAP earnings in Q1 2026. Looking at the data from the major MSR brokers, the true value of MSRs in the market today is closer to 4.8x on conventional servicing assets and 3.8x on Ginnie Mae MSRs.

If UWMC were forced to sell their MSR, that would imply a ~ 50 bps write-down (over $1B) and could wipe out two-thirds of the company’s equity. If UWMC had more rational pricing, the production volumes would fall but secondary market profitability would probably increase – both for UWMC and the entire industry. But remember that the Countrywide model is to use loss leader pricing for loans to drive out competition. As one issuer told The IRA last week, if UWMC disappeared tomorrow, gain on sale margins in the industry would at least double.

While Ishbia claims that the acquisition of TWO was about increasing the UWMC servicing book, in fact the motivation seems to be accessing a new source of liquidity to offset mounting operating losses. We find the hyper aggressive UWMC business model to be unstable, unsustainable and remarkably similar to pre-crisis Countrywide. The big difference between 2008 and 2026, of course, is that residential mortgage rates may not go down significantly for some time.

PennyMac Financial

This week saw several other important earnings announcements from the mortgage sector, including PennyMac Financial (PFSI) and Rocket Mortgage (RKT). Both saw better volumes in Q1 2026 and a mark down of mortgage servicing rights due to lower interest rates in the first two months of the quarter.

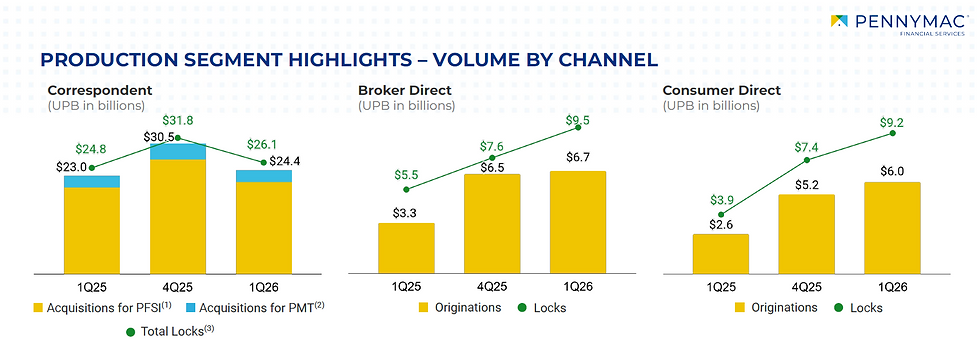

Rebounding from the disastrous Q4 2025 earnings release, PFSI reported a mixed first quarter of 2026, with Q1 net income of $82.3 million ($1.53 per diluted share) missing analyst expectations. Adjusted EPS of $2.19 fell short of estimates, largely due to weaker servicing results and hedging losses. Strong production segment earnings, which hit a five-year high, helped offset these losses. PFSI pushed up volumes in the broker channel, where they are head to head with UWMC, as shown below.

PennyMac Financial

Source: PFSI (Q1 2026)

PFSI’s servicing book was essentially flat in Q1. Production volume was more than offset by $26 billion in runoff from prepayments and the previously-announced sale of $24 billion in UPB of MSRs that transferred early in 1Q 2026. The fair value of the PFSI MSR was $10.1 billion at the end of Q1 2026, reflecting a change in the modelled valuation of less than 2%. Compare that to the double digit increase in the valuation of the UWMC MSRs noted above.

The Rocket Companies

Rocket Companies delivered strong first-quarter 2026 results, beating Wall Street expectations with $2.94 billion in total revenue and a GAAP net income of $297 million. The company saw significant growth compared to a net loss of $212 million in the same period last year, fueled by a 19% sequential increase in net rate lock volume to $49 billion. RKT ended the quarter with $19.3 billion in MSRs and $2.6 billion in cash.

Rocket Companies | Q1 2026

The table above shows the dramatic impact of the merger with Mr. Cooper in Q3 last year, leading to a 3x growth in revenue and EBITDA. Today RKT has twice the MSRs of JPMorgan (JPM) and far better liquidity and profitability than any other nonbank issuer in the mortgage sector. The change in the fair value of the RKT MSR in Q1 2026 vs Q4 2025 was less than 1%. Of course the success of RKT is very much a joint effort, but we give a big hat tip to Jay Bray and the Mr. Cooper team.

Rocket Companies | Q1 2026

While we don't own securities in any of the nonbank mortgage issuers because of our extensive work in the industry, we do think that RKT and PFSI offer some interesting value for investors after the sharp selloff in Q1 2026. But we do not expect to see short-term interest rates fall for most of this year due to the inflationary impact of the Iran war.

That said, in the event that a lasting cessation of hostilities does occur between the US and Iran, we will likely see a sustained rally in longer-term interest rates. The demarcation point for an increase in mortgage lending volumes is a about 4.1% yield on the Treasury 10-year note, as shown in the chart below.

Source: dataQollab

The Institutional Risk Analyst (ISSN 2692-1812) is published by Whalen Global Advisors LLC and is provided for general informational purposes only and is not intended for trading purposes or financial advice. By making use of The Institutional Risk Analyst web site and content, the recipient thereof acknowledges and agrees to our copyright and the matters set forth below in this disclaimer. Whalen Global Advisors LLC makes no representation or warranty (express or implied) regarding the adequacy, accuracy or completeness of any information in The Institutional Risk Analyst. Information contained herein is obtained from public and private sources deemed reliable. Any analysis or statements contained in The Institutional Risk Analyst are preliminary and are not intended to be complete, and such information is qualified in its entirety. Any opinions or estimates contained in The Institutional Risk Analyst represent the judgment of Whalen Global Advisors LLC at this time, and is subject to change without notice. The Institutional Risk Analyst is not an offer to sell, or a solicitation of an offer to buy, any securities or instruments named or described herein. The Institutional Risk Analyst is not intended to provide, and must not be relied on for, accounting, legal, regulatory, tax, business, financial or related advice or investment recommendations. Whalen Global Advisors LLC is not acting as fiduciary or advisor with respect to the information contained herein. You must consult with your own advisors as to the legal, regulatory, tax, business, financial, investment and other aspects of the subjects addressed in The Institutional Risk Analyst. Interested parties are advised to contact Whalen Global Advisors LLC for more information.

Comments