The Curse of Humphrey Hawkins

- Feb 14, 2022

- 6 min read

And now, Master, I myself invite you

To drain this vessel

In which smokes and bubbles

No longer Death, no longer poison, but life!

MÉPHISTOPHÉLÈS (Faust Libretto)

February 14, 2022 | A big Happy Valentine’s Day to all of the readers of The Institutional Risk Analyst. We all just spent the past week watching the slow destruction of the remaining credibility of the Federal Open Market Committee, a big problem for global equity markets that trust in the judgment of central bankers. The messy situation at the Fed begs the question: Is it time for Congress to repeal the Humphrey-Hawkins law?

Part of the challenge to understanding Fed policy is that the central bank has very publicly lost its way. In an attempt to parse the “FedSpeak,” as he so aptly calls it, Steve Liesmann at CNBC has begun to rely on the language of the schoolyard to explain Fed behavior – or lack of it. But alas, there are no “take backs” or “do overs” in global finance.

In fact, as Liesmann and others have noted, the Fed has still not changed policy since the start of the year. What's the fuss? The FRBNY is still buying billions of new MBS each week, even as the mortgage industry is reeling from a decidedly weak fourth quarter. A quick look at the Bloomberg terminal reveals that bond issuance in many markets is slowing as 2022 begins.

Source: SIFMA

Long-term interest rates are already headed higher, a fact that is having a big impact on less efficient home lenders. New age mortgage firm Better.com, for example, just revealed a $111 million loss in the first nine months of 2021, driven by – wait for it -- $1 billion in “corporate expenses,” Inside Mortgage Finance reveals. Does this include that trip to Pebble Beach for dozens of industry operators and biz dev moguls?

Better.com is just one of dozens of new age enterprises that are happily destroying shareholder value c/o the FOMC. And the FOMC continues to ease policy even as February draws to a close. Notice that the aggregate mortgage related issuance in November and December was the lowest monthly rates in years.

More important, notice the sharp decline in Treasury and also corporate issuance in Q4 2021 after the Treasury rebuilt its cash reserves. In January, the Treasury actually ran a surplus. During this period, the Fed did not adjust its purchases for the system open market account (SOMA), helping to force real interest rates ever more negative. If you consider QE “stimulus” inflationary, then Fed policy actually accelerated inflation in the November-January period.

The big deficit at the FOMC, of course is nerve. Having allowed themselves to climb down into the mosh pit of partisan politics during COVID, the central bank is now faced with a clear rebuke from markets and consumers in terms of inflation. Rising prices are a political problem for the White House and Congress, but the Fed has already traded that coin.

Getting “ahead of the curve,” as Fed staffers now claim to want, is unlikely with the Fed’s toolbox so badly depleted. Note, though, that the FOMC continues to drag its feet on changing policy. It’s almost as though Powell & Co expect to awake from a bad dream and find that inflation is no longer a problem.

Reserve Bank Presidents such as James Bullard and Ester George are publicly calling for a radical change in monetary policy. Sadly, the hawks on the FOMC have no choice but to speak publicly when the FOMC has gone so badly off the rails. The lack of clarity on the Fed’s legal mandate contributes to an atmosphere of confusion in the markets.

Governors and Reserve Bank presidents conduct media interviews as and when they so choose. In the days of Chairmen like Paul Volcker and even Alan Greenspan, the chairman spoke publicly and presented the consensus position of the Committee. Other FOMC members were silent unless and until they were asked to carry the consensus message. Legendary staff chief Ted Truman would have it no other way.

Today, by comparison, we have policy chaos at the Fed, with FOMC members scored via dot plots and competing with one another for media attention. Whatever consensus exists among FOMC members as to the dual mandate of Humphrey Hawkins is unclear. Meanwhile, the FOMC is clearly not fully in command of the little operational details like how to end QE.

Since 2008 and the term of Chairman Benjamin Bernanke, the Fed has lost its way, both in terms of policy implementation and as an organization. As the Fed’s public credibility ebbs, the markets sense the lack of direction and certainty of purpose, resulting in even greater uncertainty and market volatility. Notice that market volatility measured by the VIX has increased during the period of extraordinary asset purchases via QE.

Likewise the volatility of the Treasury market has also increased as the SOMA portfolio has grown. Keep in mind that the assumption by the FOMC in approving "going big" via QE was that a surfeit of liquidity would eliminate the need to "fine tune" the market. Yet the opposite seems to be the case.

Part of the problem, of course, is that most investors and media are focused on the equity markets. The Fed’s manipulation of the bond market via QE, on the other hand, is an abstraction. We’ve started counting the number of times that media and investment professionals opine that the Fed is going to start selling securities. In fact, nothing like that is in the cards. The fact that smart investors and media don’t understand this nuance is telling.

When the Fed does finally, belatedly react to the change in inflation indicators over the past six months, it will need to “go big” in terms of target rates simply to regain some degree of credibility. Just as the Fed went “big” with QE in 2020 in the face of the uncertainty of COVID, now the central bank must claw back some modicum of authority by going the other way. But, again, the most daring policy likely to come from the FOMC is merely ending new purchases and allowing the Fed’s $8 trillion portfolio to slowly run off.

Fed Chairman Arthur Burns noted in August of 1971 that he had failed to stop the closing of the gold window, reckoned as one of the more significant events in the history of the dollar in the post-WWII era. Yet the decision to end gold convertibility of dollar was relatively passive.

“The gold window may have to be closed tomorrow because we now have a government that seems incapable, not only of constructive leadership, but of any action at all,” Burns wrote in August 21, 1971. “What a tragedy for mankind!”

Half a century ago, the inflationary pressures that caused the US to stop redeeming dollars for gold at $35 per ounce were growing, with seven dollars outside the country for every dollar’s worth of gold at Fort Knox. Today the 147.3 million troy ounces of gold in Fort Knox is worth about $270 billion, but offshore dollar assets are measured in double digit trillions of dollars.

In 1971, people inside and outside the US government still believed that it was possible to create real economic outcomes via government fiat, all the while maintaining low inflation. Burns talked of an “incomes policy,” trading higher wages for productivity gains even as President Richard Nixon embraced wage and price controls to offset the inflationary impact of the Vietnam War.

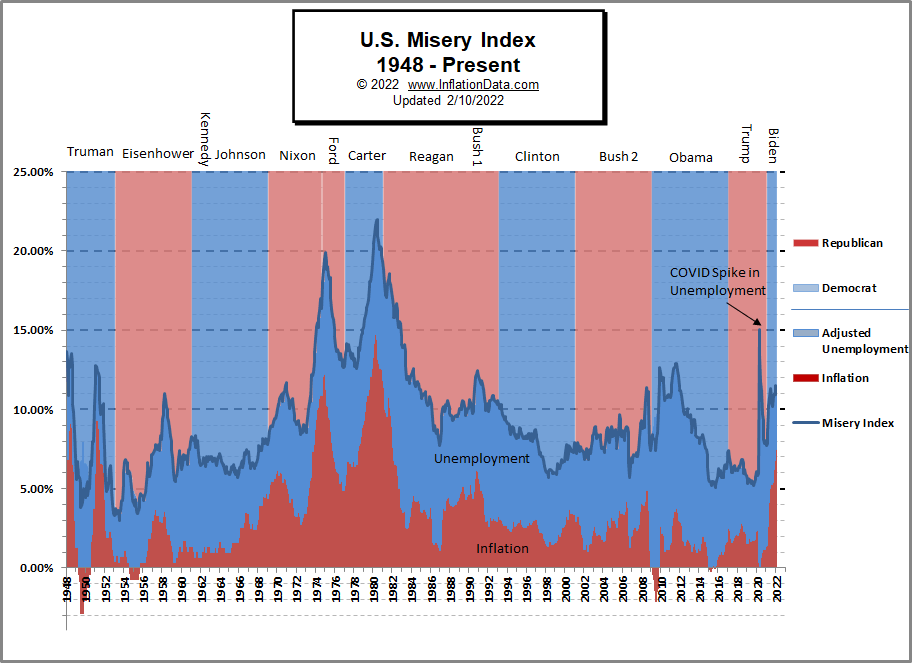

In 1978, when Congress passed the Humphrey Hawkins law, the mandate for full employment and price stability was enshrined within the Federal Reserve Act. This political compromise juxtaposed jobs vs inflation, a conflicted relationship that cannot be managed either practically or politically. When the Fed could no longer deliver the goods after 2008 by just lowering interest rates, buying government debt became the policy tool of choice.

As we noted in American Conservative (“When The Fed Became A Socialist Job Creator’), the Fed is a progressive, New Deal institution. And Humphrey-Hawkins was an explicitly socialist law imposed by a Democratic majority in Congress that must inevitably lead to inflation. When Fed Chairman Bernanke tried to differentiate between credit easing and QE in a 2009 speech in London, the world witnessed the last gasps of the dual mandate.

Since 2009, QE has delivered monumental inflation, this justified in the name of short-term expedience that make a mockery of the “price stability” portion of Humphrey Hawkins. The FOMC during the terms of Chairman Bernanke, Chair Janet Yellen and now Jerome Powell document the consensus view at the Fed over the past decade or more that “inflation is too low.”

The first impact of QE was asset price inflation, a sea of institutional liquidity that enabled ridiculous behavior in the world of asset creation and allocation. Ponder the shift in investor perception that made investments such as better.com seem like a good idea. And there are literally hundreds of other companies that share this quality – or lack thereof. We’ll be writing about some of these names in coming weeks.

But in the meantime, enjoy the ride in the financial markets over the rest of 2022 as the Fed seeks to reclaim virtue when it comes to fighting inflation. The markets will shoulder the burden, this even though few bankers or equity managers yet perceive the adjustment that lies ahead.

One wealthy business owner told The IRA last week: “If the Fed does the right thing now, I will loose 25% of my net worth due to the obvious and necessary reset in stocks, but that’s OK. I’m still up a lot. But if Powell doesn’t take strong action now to control inflation, then we are all in big trouble.”

Comments