Loan Delinquency, EBOs & Ginnie Mae MSRs

- Nov 15, 2022

- 6 min read

Updated: Nov 16, 2022

November 15, 2022 | Premium Service | The annual migration of industry professionals to the IMN MSR East conference in lower Manhattan was well-attended and instructive, though not without some intense debate among participants. The longs are getting a tad bloated as valuations rise, but the shorts in the equity markets are spending a lot of capital to prove they’re right. We'll see.

One of the more amusing impressions from the meetings were reports that our friends at Ginnie Mae continue to search for the magic formula that will encourage depositories to return to government lending and particularly servicing. Given the risks facing depositories from both mortgage securities and loans, don’t hold your breath. Banks will happily originate high-FICO FHA loans with 7s and 8s and retain same in portfolio, but will never return to the Ginnie Mae MBS market because of the high cost of servicing government loans.

Another entertaining snapshot came when a representative of the Council of State Bank Supervisors essentially threw Ginnie Mae under the bus, noting that the CSBS aligned its recommendations for nonbank capital with the Federal Housing Finance Agency. The CSBS representative then repeated concerns about possible mark-to-mark losses for MSRs owned by banks and nonbanks alike arising from implementation of the Ginnie Mae risk-based capital rule. A number of participants at the IMN event echoed these concerns.

It seems obvious that the reported book value metrics coming from many commercial banks, REITs and mortgage banks are a tad inflated, but not to the Buy Side community. Watching Two Harbors (TWO) completing a 1:4 reverse stock split only adds to the aspirational atmosphere in the sector as layoffs accelerate each month. Leading non-QM loan shop Angle Oak (AOMR) has exited the retail channel and Finance of America (FOA) has likewise retreated from the forward loan market.

Annaly Capital Management (NLY) is trading near 0.9x tangible book value and Rithm Capital is (RITM) is just above 7x, but how much more should these valuations be adjusted down to account for overvaluation of mortgage servicing assets? NLY’s $1.7 billion in all conventional MSRs are booked at a 5.4x multiple as of Q3 2022. In a forced secondary market sale, these MSRs would likely go for a full multiple below these levels.

Here’s the problem. With prepayment rates now below 5% CPR, there is not a lot more room for MSR values to expand. As owners of MSR try to increase the collateral value of the asset, one CEO tells The IRA, you need negative prepayment rates to make the numbers work. Meanwhile, Ginnie Mae is threatening to drive leverage ratios back a decade to 50% on the fair value of MSR, a move that all of the participants agree will end in tears.

Meanwhile, some of the more aggressive third-party valuation shops are backpedaling on assessment as the Treasury market rallies more than it has in years. Volatility is no one’s friend in this market, with shifts in the Treasury yield curve accounting for the lion’s share of the market risk.

“The Fannie Mae 30-year current-coupon spread to the 5/10-year blend tightened 25 basis points to +141 as the US Treasury 10-year yield fell 28 basis points to 3.81% and volatility was little changed,” Bloomberg reported this week. “The spread decreased the most in more than two years. Yields on Treasuries saw the biggest decrease in more than two years.”

We’ve noted before that this sort of market volatility renders attempts to hedge securities or loans effectively useless. But the big takeaway from the IMN conference were the reports of lenders, banks and IMBs alike, that are still coming to grips with what the FOMC has done to the mortgage markets. As one Ginnie Mae issuer asked on a government blog: “Does the FHA expect us to take a 20-point loss selling a reperforming 3% loan?” The answer to that question is most definitely yes.

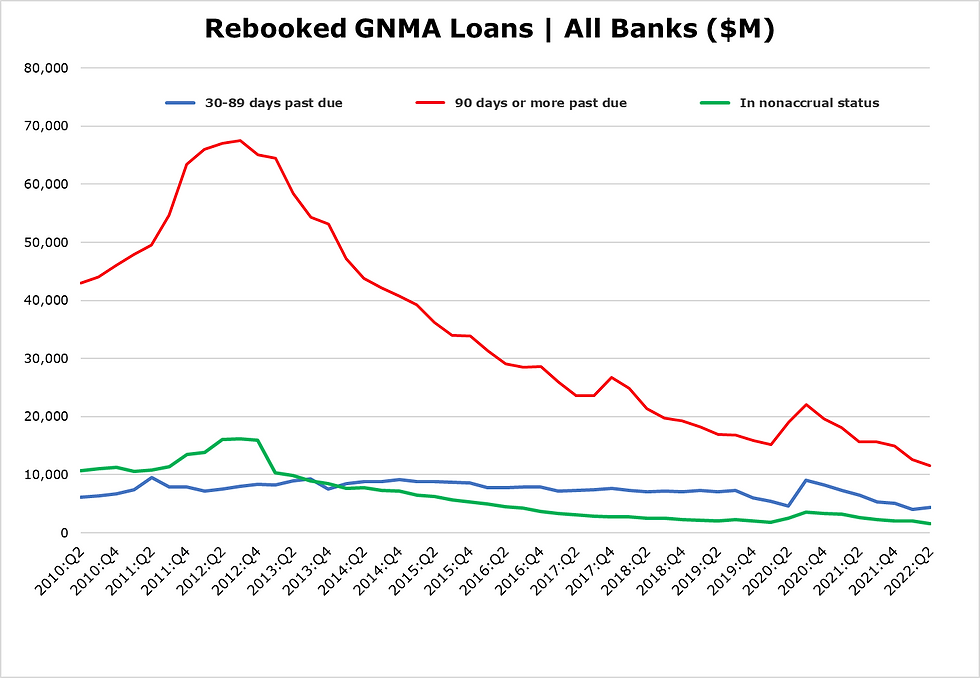

There are a surprising number of banks and nonbanks that are holding early-buyouts (EBOs) of delinquent loans that are in process of modification. Once these loans are again performing, they must now only be held for three months of seasoning before the loan can be sold into a new GNMA pool. But a 3% loan sold into a Ginnie Mae 6.5% MBS could result in a 20-point loss. No surprise that EBOs activity has slowed dramatically over 2022. And now you know why banks want nothing to do with Ginnie Mae servicing.

Source: FDIC

While many holders of EBOs are not yet selling these QE era loans, it is a pretty good bet that sales will begin in Q1 2022 from smaller issuers. When buyers return with allocations and EBOs become eligible for pooling into MBS, the proverbial decision on loss realization will be forced. In that sense, the worst possible outcome for a large holder of EBOs is timely resolution.

Our friend Dick Kazarian of MIAC reminds us that there are two components to the pricing of a loan:

Loan Spread: The primary loan rate vs the secondary market rate for whole loans, which has tightened dramatically during 2022 to just 0.87% vs 1.4% in 2020. The primary-secondary spread, excluding the gfee, can be considered the retail markup over the wholesale cost of mortgages or the secondary rate.

Swap Spread: The swap spread is the difference between the benchmark Treasury yield and the MBS debenture rate. As mentioned earlier, this shows the difference between the maturity on the Treasury yield curve and the premium MBS for a given market. “In contrast to the primary/secondary loan spread,” Kazarian notes, “we expect significant volatility in the secondary swap spread.” Ditto.

We have already highlighted the issue of mark-to-market losses on the books of banks and REITs in low-coupon securities, but another potentially larger risk awaits in the form of EBOs that are financed at 98 cents on the dollar by warehouse lenders but have a current market value in the low 80s or high 70s. It will take only one event of default that reveals this pricing disparity to cause a fundamental re-pricing of delinquent government loans and the related servicing asset.

Source: MBA

The issue of the collateral value of EBOs and MSRs is important because the rate of cash advances on government loans continues to grow. While the reported levels of delinquency are still falling, in fact cash advanced on delinquent government loans is rising fast, suggesting that loan delinquency will start to rise as well.

But add the prospect of the new Ginnie Mae issuer eligibility rule in 2023 and issuers and investors will likely see lower prices for MSRs in the New Year. As we noted during the IMN panel yesterday, banks and nonbanks alike are currently planning their business strategy and operations for 2023 and beyond. Nobody has the time to wait to see what the folks at Ginnie Mae decide to do with their abortive risk-based capital rule. And it is important to remember that the Ginnie Mae rule does not distinguish between government and conventional MSRs.

If Ginnie Mae really intends to forcibly lower the leverage allowed on government MSRs, then we expect to see selling pressure across all servicing assets in Q1 2023. Strategic sales of MSRs in 2023 could overwhelm demand from normal portfolio allocations. It is interesting to note, for example, that public marks for Ginnie Mae MSRs are in the mid 4s times annual cash flows, but the private market bid is in the 3x range. How long will banks lend on EBOs and MSRs that are 20% overvalued?

More ominously, the prospect of adverse mark-to-market events on MSRs coming at the same time banks are trying to offload underwater loans and MBS could push some bank and nonbank Ginnie Mae issuers into insolvency. Between the FOMC under Jerome Powell and Ginnie May under President Alana McCargo, all mortgage issuers face a perfect storm in 2023. When interest rates do eventually decline, we'll be talking about margin calls a la 2020 on these same assets.

The Institutional Risk Analyst is published by Whalen Global Advisors LLC and is provided for general informational purposes only and is not intended for trading purposes or financial advice. By making use of The Institutional Risk Analyst web site and content, the recipient thereof acknowledges and agrees to our copyright and the matters set forth below in this disclaimer. Whalen Global Advisors LLC makes no representation or warranty (express or implied) regarding the adequacy, accuracy or completeness of any information in The Institutional Risk Analyst. Information contained herein is obtained from public and private sources deemed reliable. Any analysis or statements contained in The Institutional Risk Analyst are preliminary and are not intended to be complete, and such information is qualified in its entirety. Any opinions or estimates contained in The Institutional Risk Analyst represent the judgment of Whalen Global Advisors LLC at this time, and is subject to change without notice. The Institutional Risk Analyst is not an offer to sell, or a solicitation of an offer to buy, any securities or instruments named or described herein. The Institutional Risk Analyst is not intended to provide, and must not be relied on for, accounting, legal, regulatory, tax, business, financial or related advice or investment recommendations. Whalen Global Advisors LLC is not acting as fiduciary or advisor with respect to the information contained herein. You must consult with your own advisors as to the legal, regulatory, tax, business, financial, investment and other aspects of the subjects addressed in The Institutional Risk Analyst. Interested parties are advised to contact Whalen Global Advisors LLC for more information.

Comments