.png)

Risk & Return in the Age of Misgovernance

- Aug 11, 2020

- 5 min read

Updated: Aug 21, 2020

New York | We have returned from the Maine Woods refreshed and ready for the sprint to Labor Day. The fish were big and the bugs almost entirely absent. We put the nix on fried potatoes and wine at lunch, and visited some remarkable small lakes with really big bass. And we regret to report that the first large mouth bass was taken from the Fourth Machias Lake. The invading fish was eaten with great relish.

Of course, a large mouth bass is considered an “invasive species” in Maine and thus may be taken and eaten in unlimited numbers. But a small mouth bass is also an immigrant from southern waters, albeit from a century ago. To borrow the moniker of our friend Dan at Zero Hedge, on a long enough timeline every creature on the planet qualifies as an invader. Ponder that when thinking about economic and social justice.

A reader sends this thoughtful query:

“I recently read your 2017 article on QE and FANG stocks. Looks like things have improved dramatically since then, wouldn't you say? That is, of course, a morbid joke. My heart tells me to keep hope alive, but my head says we are on the brink of the worst global economic collapse in history. Thoughts?”

The fixation with Facebook (NYSE:F), Amazon (NASDAQ:AMZN), Netflix (NASDAQ:NFLX), and Alphabet (NASDAQ:GOOG) tells you all that you need to know about the global, that is, consumer economy. Not a single transformational enterprise in the group. All the Fang stocks, in fact, pander to the vanity and convenience of the more affluent consumer. And it is the world's desire for access to these consumers that ultimately supports the dollar. Thus falling US consumer spending is an ominous sign.

At the moment, the dollar is the global “asset” and other currencies are liabilities. Dollar stocks are an inflation hedge of sorts, while bonds are taxed by the FOMC’s targeting of federal funds as a policy instrument. As and when America’s incompetent political class convinces the world that we are unworthy of the privilege of being the world's reserve currency, then the dollar will become a liability and another medium will be the global asset and means of exchange.

Note, for example, that after the dollar spiked 10% higher in March, the broad index has given up these gains and more. Seeing Americans rioting and burning buildings in major cities does not help the value of the dollar. And as the dollar has weakened, the spreads between short-term rates in yen and euro have narrowed.

Improvement is a relative concept in a world where American elected officials have lost the ability to govern and maintain civil order. Chicago’s Democrat Mayor Lori Lightfoot, in the latest example, allowed citizens to riot and loot stores on the Miracle Mile.

“All bridges are being raised along the river throughout The Loop,” reports CBS News. “Chicago’s Office of Emergency Management announced street closures throughout areas in the Magnificent Mile, Gold Coast and South Loop.”

Meanwhile, President Donald Trump urges officials in Oregon to bring in National Guard amid unrest in Portland, and warns officials they will be 'held responsible' for destruction. See our comment in The American Conservative, "A Socialist New York Staggers Toward Default."

In the face of the misgovernance evident in many parts of American life, our dutiful central bank continues to do too much in response. And, of course, the Federal Reserve refuses to ever say no to the debauched politicians who mismanage things in Washington and elsewhere. Thus, there is copious and ever flowing liquidity in the financial markets. That is a clue.

Our friend Rob Chrisman provides this update on Treasury issuance for the rest of the year: “The US federal government will need to maintain borrowing at elevated levels as the coronavirus crisis continues, although it should decline marginally this quarter, the Treasury said. Offerings of all Treasury securities will be increased but the emphasis will be on 7-year and 10-year notes, and bonds with 20-year and 30-year maturities, as the government aims to shift to longer-dated debt.”

Of course, the Federal Open Market Committee will be purchasing a great deal of the Treasury’s debt issuance in the next several years, raising questions as to how and when the central bank will ever reduce its balance sheet. As we like to remind one and all, the problem with quantitative easing or QE is that it represents a permanent add to the Fed’s balance sheet so long as Treasury remains in deficit.

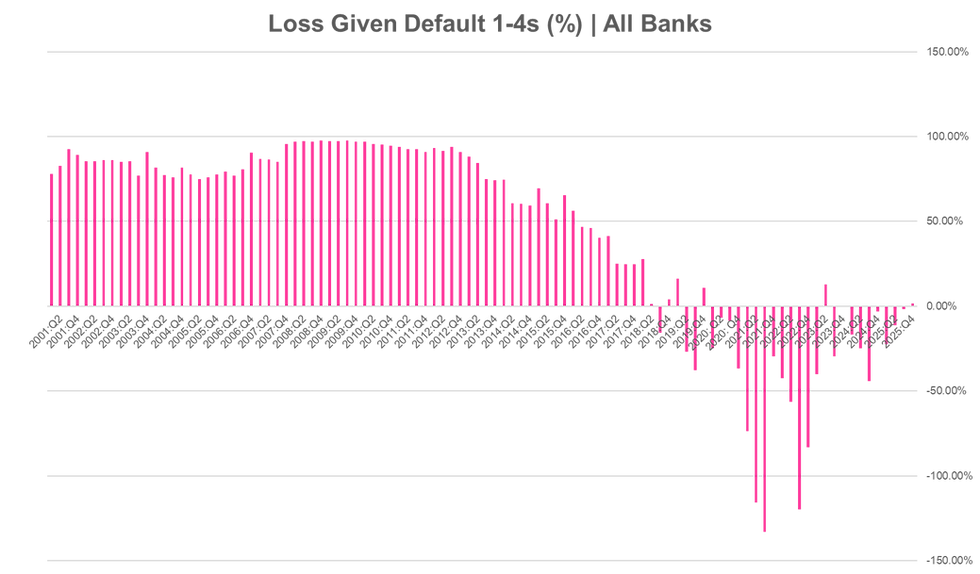

The chart below shows the system open market account (SOMA) vs the CBOE VIX Index. Notice that the VIX has still not returned to levels of Q1 2020.

The FOMC must continue to purchase Treasury and agency mortgage backed securities sufficient to maintain the size of the balance sheet and thereby market liquidity and bank deposits. Otherwise, we risk a repeat of the market volatility seen in 2019. Again, the bias in interest rates is lower for longer.

Last week, Rocket Companies (NYSE:RKT) priced at $18 per share or a $36 billion enterprise value, adding yet another name to the world of listed non-bank financial firms. The strong financials of RKT (1x leverage) and the ability of Quicken Loans to create new assets, we suspect, will make the leading mortgage lender and servicer a benchmarks in the mortgage group. We’ll be publishing a profile on RKT once some of the data settles down.

It is interesting to note that Mortgage Originators & Servicers have outperformed the S&P and other broad indices over the past month, perhaps due to the RKT IPO. But we also think that a number of investors have noticed that interest rates are low and are likely to remain low for some time. The FOMC intends to use housing as the engine of an eventual recovery in the broader economy, but that indirect method will take years to achieve success.

Thus we expect primary-secondary market spreads for residential mortgages to remain very attractive for issuers like RKT. As one leading industry MSR owner opined last week, the rich primary secondary spread (consumer loan coupon minus the MBS debenture rate) ensures that most of pre-2020 vintages will prepay. "We'll see 2.5% loan coupons," he muses.

“It's going to take years for the US economy to fully heal from the economic disaster brought about by COVID-19 and the government-mandated shutdowns which continue to limit economic activity across the country,” write FT Advisors. “When we talk about a full recovery, we don't simply mean getting real GDP back where it was in late 2019; a full recovery comes when the unemployment rate gets back below 4.0%, and we don't see that happening until at least late 2023.”

The IRA Adds Premium Service

Editor's note: For some time, readers of The Institutional Risk Analyst have been asking for a subscription offering for our company analysis service. In response, we shall be creating a paid addition to The IRA blog that will showcase company risk profiles, videos and other premium content. In addition, the online store for bank risk profiles will be going away. Look for these and other changes to go live between now and Labor Day.

The very popular Labor Day trip to Leen’s Lodge in Grand Lake Stream Maine is still on this year. There are a couple of spots available for fine end of season fishing, dining and natural beauty. For details, please contact Scott Weeks info@leenslodge.com or (800) 995-3367.

Comments