.png)

Is Multifamily Lending a Threat to US Banks?

- Nov 20, 2017

- 6 min read

Updated: Nov 8, 2021

Trump Pavilion from the Van Wyck Expressway

New York | Q: Besides stocks, what asset class has benefitted the most from the radical monetary policies of the Federal Open Market Committee? A: Multifamily real estate. And what asset class most worries federal bank regulators today? Same answer.

By means of introduction, multifamily real estate in major urban areas has been one of the most popular and solid asset classes for US banks historically going back to WWII. Family fortunes, including that behind Donald Trump and many other New Yorkers, started in the 1950s with multifamily housing in Manhattan, Queens and the other boroughs of New York City. Net loss rates on these assets, measured over years and decades have been among the lowest of any bank loan category, but short-term changes in valuation in the 1990s and 2008 were severe.

Since the passage of the 2010 Dodd-Frank legislation, regulators have made some draconian changes to limits on bank loan types and loan-to-value (LTV) ratios that, some say, are stifling responsible lending and make little sense from a credit perspective. Most recently, federal regulators have proposed regulations that replace the high volatility commercial real estate (HVCRE) regulations with a new and much simpler High Volatility Acquisition, Development and Construction (HVADC) exposure, a measure that incorporates more risk from construction and development loans.

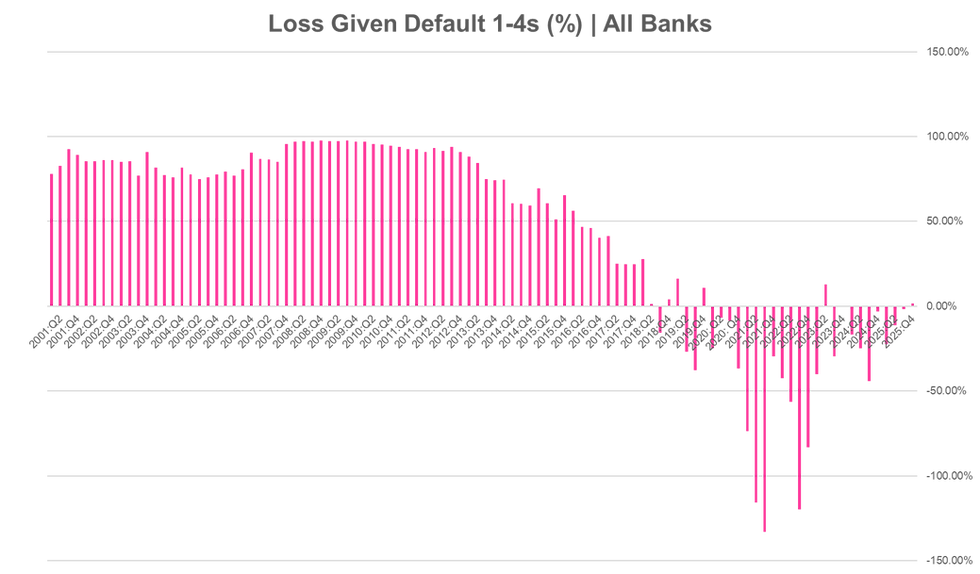

Is all of this concern warranted? Yes. Thanks to the folks who sit on the FOMC, prices for multifamily real estate have risen so rapidly since Dodd-Frank that today net default rates are actually negative. As we’ve noted in previous missives, loss-given default (LGD) for the $400 billion in multifamily loans held by US banks is negative in four of the past six quarters. In plain terms, banks are profiting from defaults on multifamily loans because collateral prices have risen so rapidly, as shown in Chart 1 below.

Source: FDIC

In the world of analytics, a negative net default rate is a “red flag” because it indicates that markets have reached an outlier position that cannot be sustained. The negative loss rates post-default seen today contrast with the 100% LGDs that applied during the 2008 financial crisis. Even going back to the economic slowdown of the late 1990s, LGDs on bank multifamily exposures were relatively high.

Yet as an asset class, multifamily bank loans have been among the most stable credits on the books of US depositories, especially community banks in major urban metro areas. More, while bank portfolios for multifamily loans have been stable, the overall flow of funds into multifamily assets via the asset-backed security market has surged during the period of low rates and “quantitative easing,” as shown in Chart 2 from FRED.

Source: FRED

Often times the most powerful limits placed on banks are not contained in statutory provisions, but in the guidance institutions receive from regulators. For the past couple of years, the Office of the Comptroller of the Currency has been giving cautionary guidance to banks and thrifts about lending on multifamily real estate in major urban areas, especially multifamily rental properties. We are talking here about Washington DC, New York, Los Angeles and Dallas, among the major urban metros. The guidance for smaller banks was that such exposures should generally not exceed 300% of tier one equity capital.

Ironically, the concern of prudential regulators in multifamily housing is driven by the actions of another set of regulators acting on the FOMC. Multifamily real estate as an asset class has been among the most effected by the FOMC's manipulation of credit spreads and asset prices of the past decade. Prices for high end real estate in major metros such as Denver, Seattle and Austin have soared in recent years, fueled by low interest rates and ready supplies of private equity capital sitting on the sidelines. Ed Pinto at AEI sent us Chart 3 below, which compares the growth rate of total debt with multifamily rental units.

While loan-to-value ratios for urban multifamily properties have actually fallen since the crisis, dollar exposures to banks have risen with valuations. In response, regulators and particularly the OCC have been restraining community banks from exceeding the 300% guidance in terms of total exposures. Indeed, it has been made very clear to national banks who lend on small, rental and owner-occupied commercial properties that they cannot exceed the guidance. The 300% guideline on in-town multifamily assets is in fact a cap.

As the OCC noted in 2015: “Although the underwriting for loans that finance these smaller properties is similar in many respects to the underwriting for loans that finance larger properties, there are important differences that are useful to consider. The biggest difference is often the borrower. These borrowers often have less experience and fewer resources than investors in larger properties.”

Since that time, however, the OCC’s views have apparently hardened, bankers tell The IRA, especially in the past year. The vehicle for delivering the message to banks is the examiner in charge of inspecting that institution. This “informal” guidance has significant weight, however, and illustrates some of the subtle issues that Republicans are hoping to address in Washington as they take control of agencies such as the OCC as well as through regulatory reform.

Because of the OCC’s conservative stance, state chartered banks that focus on commercial lending have a big advantage over national banks. When state regulators and the Federal Deposit Insurance Corporation work with state-chartered institutions, they typically allow a bank to exceed regulatory guidelines if that bank shows the ability to manage credit risk.

A good example of such an institution is state-chartered Bank of the Ozarks (NASDAQ:OZRK), a national lender that leads its peer group in terms of credit performance. The bank is shedding its bank holding company, meaning FDIC is the sole federal regulator for this commercial lender. This gives the state-chartered OZRK a decided advantage over national banks its size or larger.

It needs to be stated that the OCC’s caution regarding commercial real estate is well-considered given the froth in all types of real estate. Increased asset prices for commercial real estate have caused a commensurate increase in the dollar amount of loan exposures even as LTV ratios have fallen since the 2008 crisis. Whenever prices for real estate are rising at a rate far higher than the underlying economic growth rate, caution is advisable.

That said, multifamily and related commercial loan exposures at all US banks are performing extremely well. The $400 billion in bank loans secured by multifamily real estate held by US banks showed a tiny 0.15% non-current rate at the end of Q2 ’17 and charge-offs were essentially zero. Looking back to the 1990s, multifamily loans have gone through periods when non-current rates have risen sharply as shown in Chart 4 below.

Source: FDIC

But net losses after default have been extremely low, both in the 1990s and more recently. This was largely because these properties are so widely sought after by local investors. With LTV ratios for multifamily assets in the 50 percent range and falling, it also needs to be said that the intensity of the OCC’s focus on risk from multifamily loans in large markets such as New York seems overdone.

Not only did multifamily loans perform better than most other real estate asset types during the 2008 financial crisis, but the equity behind these loans has basically not gone down in half a century. This point is especially powerful when you consider that the agency is at times recommending that national banks substitute unsecured commercial loans for fully secured loans on multifamily real estate. We hear that it has even been suggested to some banks by OCC personnel that commercial real estate lending on beachfront property is preferable to loans on multi-family rental properties located in cities such as Seattle and Miami. Really?

In order to accept as true the OCC’s apparent position that multifamily loans pose a threat to the safety and soundness of US banks, you’d need to expect that valuations for these liquid and popular real estate assets are about to be cut in half. In fact, the default and recovery statistics for multifamily real estate loans held by banks and in ABS suggest just the opposite, that there is a strong market for assets that do default and that prudently run credit exposures in these assets have considerable protection against loss given those rare default events.

While there is certainly reason to be concerned about the sharp upward move in prices for all manner of real estate given the FOMC’s extraordinary policy actions, residential real estate in major urban centers is decidedly not a source of risk for banks and thrifts. Leveraged loans? Unsecured commercial credits? Sure. The real issue illustrated by frothy real estate markets is not the safety and soundness of banks, but rather asset price inflation caused by the low interest rate policies of the FOMC.

Comments